|

|

|

|

|

|

|

New Macromonitor Resources Construction Outlook: Minerals construction is well into an upturn, LNG construction to recover from 2022/23, but long term prospects for coal are limited

|

|

|

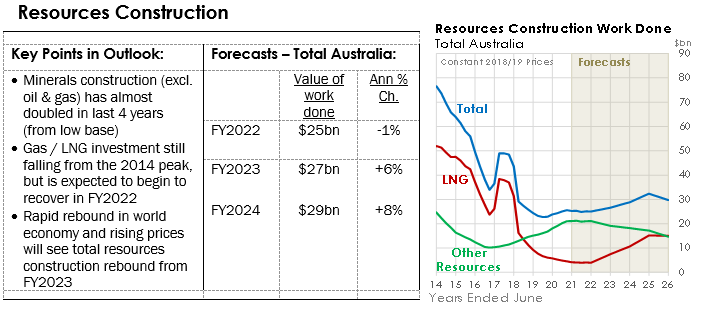

The latest forecasts from our new report, Australian Construction Outlook – Resources, show that construction in the resources sector is a tale of two segments. Firstly, resources construction excluding LNG has doubled in the last 4 years and provided short-term strength to the overall sector. Secondly, LNG investment has been falling since its 2014 peak, and more recently has faced further downward pressure from COVID-19 induced business uncertainty and price volatility. This note provides an overview of these two investment cycles.

|

|

Oil & Gas: Incredible downward pressure has been placed on the oil, gas & other hydrocarbons (oil & gas) sector, underpinned by two headwinds; the COVID-19 pandemic and last year’s geopolitical price war.

|

Crude oil prices averaged between US$60 and US$70/bbl from January 2017 to December 2019. Prices plunged during the early months of 2020, reaching an extreme low point of below US$20/bbl in April 2020. COVID-19-related restrictions on movement and activity caused large falls in oil demand, and this was compounded by an oil price war between Saudi Arabia and Russia, which caused historic falls in the oil price.

|

The ensuing oil glut and large price declines have large effects on the industry and have led to a host of projects being delayed. Work done in the oil and gas sector fell by a further 40% in 2019/20 and 30% in 2020/21.

|

Oil prices have since edged higher, prices in December 2021 just surpassed US$72/bbl, with the price increases due to a rebound in global demand and bullish expectations about growth through the first half of 2022 surpassing fears of the Omicron coronavirus variant hurting global consumption. Additionally, stimulatory fiscal and monetary policies, and vaccine roll-outs are improving economic growth and expectations.

|

|

We expect the next upturn in oil & gas construction to begin in 2022/23, climbing back close to $10 billion per year by 2023/24 and reaching a peak of $15 billion in 2024/25. This, however, pales in comparison to the peak of the last cycle, which reached over $50 billion in the mid-2010s.

|

|

|

Other Resources: Meanwhile, outside the gas sector, recovery in construction is well underway. Total resources construction, excluding oil & gas, increased by 20% (in real terms) in 2020/21, and has doubled from the low point in the cycle, which was in 2016/17. The momentum continued in 2021/22 and we expect a further 20% annual growth rate in the year to June 2022.

|

Strong construction in minerals, driven largely by iron ore projects, is the main contributor to growth. The better than expected rebound in the world economy, post the initial 2020 global restrictions, has caused improved demand for minerals and has lifted most commodity prices. Although activity is set to edge lower beyond 2022, levels of work done are expected to remain reasonably high.

|

|

Projects in some selected other commodity groups are also expected to contribute to growth in construction work, most notably, gold, rare earths, copper and cobalt.

|

|

|

Construction of coal projects is expected to decline for the third consecutive year in 2021/22 , as a result of weaker demand growth, for both coking and, in particular, thermal coal. Australian coal exports are expected to remain weak, largely due to lower shipments to China and India, both of whom are likely to favour local suppliers in the context of weaker demand.

|

Coal construction work should recover in 2023/24. In the long term, the case for new coal mines is undermined by increasing international climate action ambition and continuing declines in the price of renewable energy. These shifts are reflected in our long term forecasts, the average annual value of work done throughout our forecast period (to June 2031) is estimated to be $4.8 billion per year, which is much lower than the $8.5 billion per year in the decade prior.

|

|

The beginning of 2022/23 is likely to be the peak for non-gas related construction, with a decline to follow. By this time however, the recovery in oil & gas will be well underway. As such, the total resources construction sector is expected in peak in 2024/25.

|

|

|

For more detailed forecasts and analysis, please subscribe to our report - Australian Construction Outlook – Resources – December 2021.

|

|

|

|

|

Our most recent reports:

|

|

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|