|

|

|

|

|

|

|

Australia's data centre capacity forecast to pass 5000MW by 2029/30

Rapid increases in demand for AI and cloud infrastructure have led to an acceleration in data centre investment

|

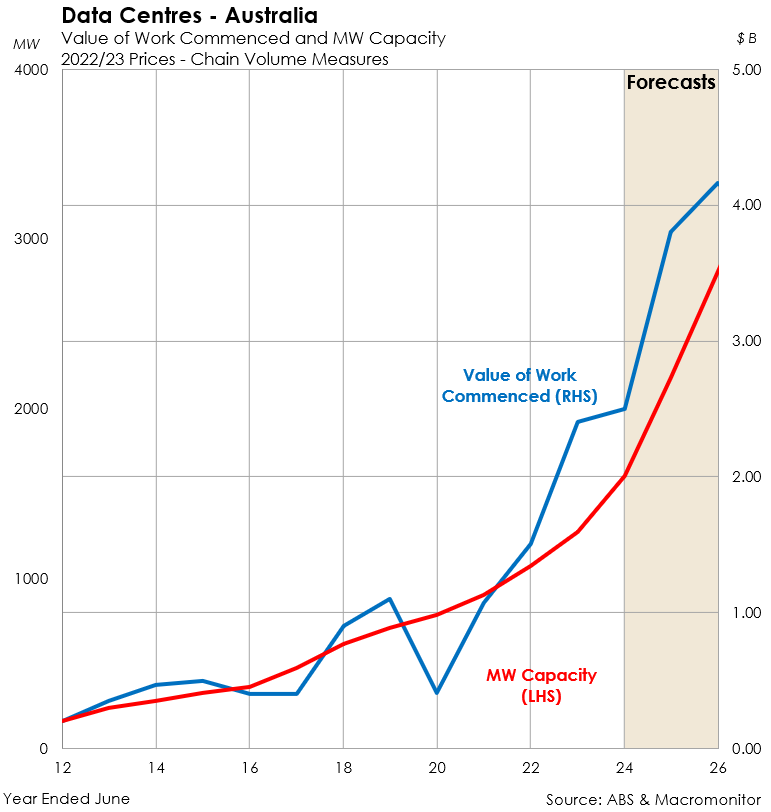

Demand for data centres has been persistently increasing since the pandemic, thanks to the proliferation of work from home, cloud computing and, most recently, artificial intelligence. Data centre building activity increased, on average, by 68% per year over the four years to June 2024. The newly released July 2025 edition of Macromonitor's Data Centre Construction Outlook report estimates that construction commencements increased a further 52% in 2024/25, with a more moderate 10% increase forecast for 2025/26.

|

The new report provides detailed forecasts of data centre construction and capacity by year, looking ahead to 2033/34. We also provide detailed breakdowns by geographic areas and lists of individual projects.

|

|

Supply, measured in megawatts (MW), is estimated to have reached 2180MW in 2024/25, a 250% increase from 2020 levels. As construction continues to ramp up, forecasts indicate that total capacity will be 2800MW by 2025/26 before crossing 5000MW in 2029/30.

|

|

|

|

In 2025, significant investment flows continued, Amazon has almost doubled its planned spending on AI, to $20 billion across Sydney and Melbourne through to 2029. Microsoft is continuing its $5 billion program and domestic players continue to expand as supply outstrips demand for the foreseeable future.

|

However, there are concerns surrounding the ability to meet electricity demand during peak times on the east coast if all proposed data centres are constructed, especially as Australia undergoes transition to renewables. 100% uptime for data centres is a requirement, hence grid instability could be a very real limitation for investment and the construction outlook for data centres.

|

|

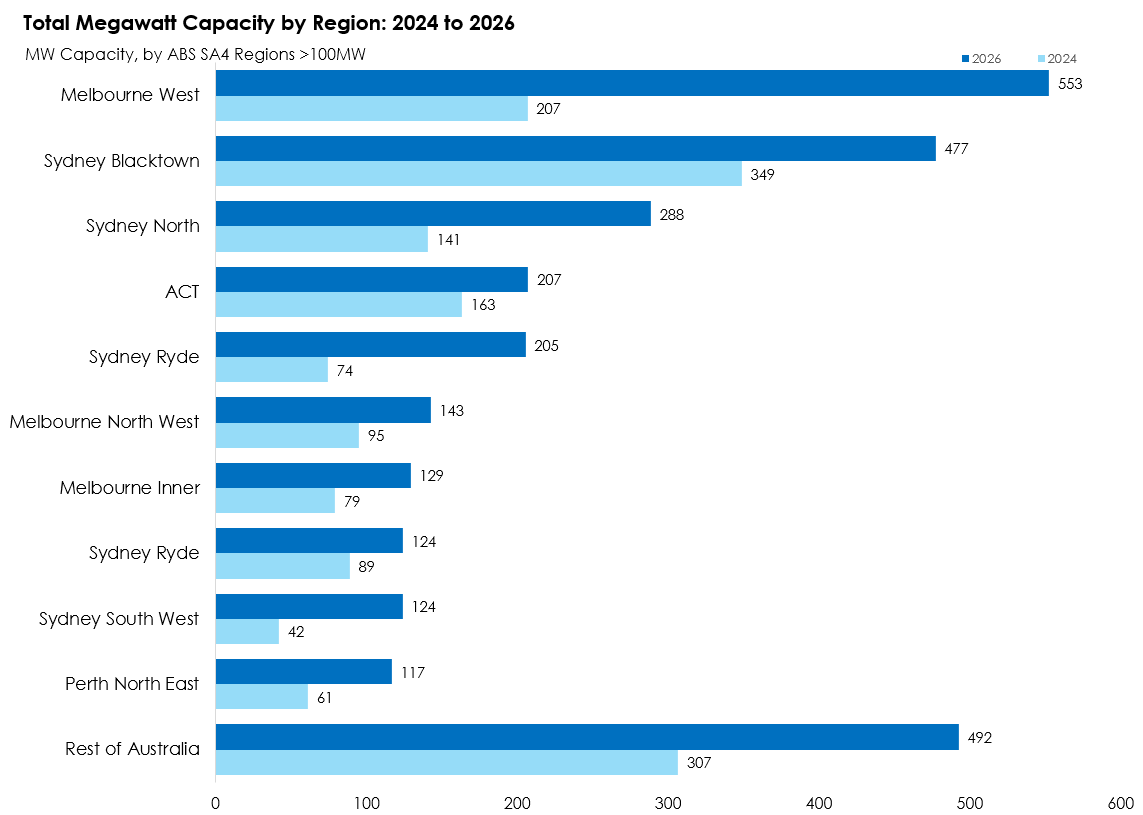

Looking closer at the distribution of data centres across Australia, there are roughly 8 regions in Sydney and Melbourne that house the overwhelming majority of all data centre construction. Of these regions, most surround the city centres and have access to all necessary infrastructure including land, fibre internet, electrical and water infrastructure. Sydney's Blacktown and Ryde regions and Melbourne's West are poised to see the most construction over the next decade.

|

|

|

|

Some major projects that have commenced or are in the pipeline include:

|

- CDC Marsden Park Campus, Sydney

- NextDC S7, Sydney

- STACK Infrastructure 78 Lockwood Road, Sydney

- CDC Laverton Campus, Melbourne

- NextDC M4, Melbourne

|

Please get in touch with us if you have any enquiries.

|

|

|

|

|

|

Our most recent reports:

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|