|

|

|

|

|

|

|

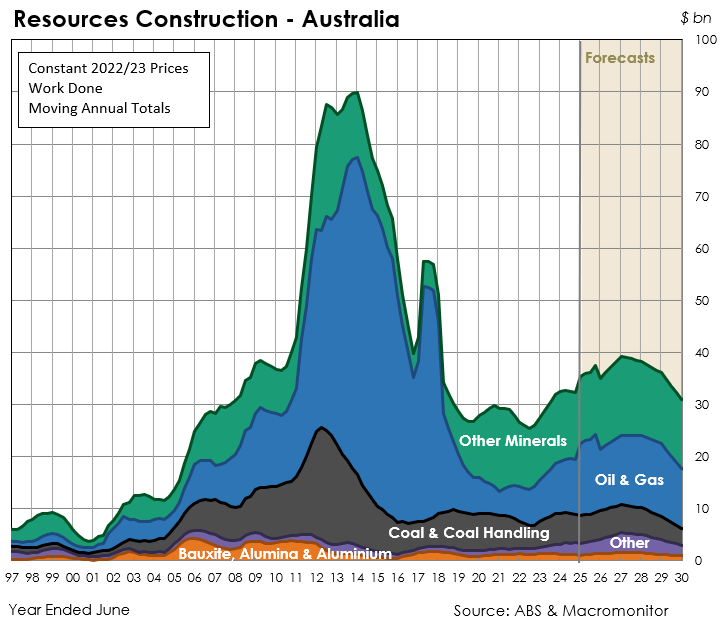

Resources construction is midway through a broad-based upturn - set to peak in 2026/27

Oil and gas dominate the upswing, with solid contributions from critical and other mineral sectors

|

Australia’s resources construction sector has grown strongly over the past three years, rising by around 33%, driven largely by a rebound in oil and gas activity and solid gains across other minerals sectors, including critical minerals. Together, the 'oil & gas' and 'other minerals' sectors accounted for about 75% of total resources construction in 2024/25, with oil and gas contributing 39% and other minerals 36%. Both sectors are expected to remain the leading contributors to activity over the next five years.

|

|

Growth is expected to moderate slightly in 2025/26 before rising to a peak in 2026/27. The upturn will be driven by a wave of gas and LNG project commencements along with new gold, copper, and critical minerals developments. A series of one-off heavy industrial processing projects, particularly in green steel, ammonia, and urea production, will further contribute to the peak.

|

|

|

Oil and gas construction has been the key driver, rising nearly threefold from $4.6 billion in 2020/21 to around $13.9 billion in 2024/25. This growth has been supported by major LNG life-extension projects and gas field developments. Meanwhile, other minerals, including iron ore, gold, and copper, have expanded as developers capitalized on strong commodity prices.

|

The critical minerals segment temporarily softened in 2024/25, with some projects delayed or scaled back due to sharp price declines for lithium, nickel, and cobalt. Despite this, policy momentum remains strong, supported by the Future Made in Australia Act and the US–Australia Critical Minerals Agreement, which aim to boost domestic processing and strengthen supply chain resilience. As a result, the sector is well-positioned for robust growth in the coming years.

|

Although the overall upturn in resources construction will be smaller than the mining investment boom of the 2010s, it will be broader-based, reflecting diversification toward low-emission energy and critical minerals. While coal-related activity will continue to decline, gas investment is expected to grow modestly, supported by its use as a firming fuel in electricity networks and as a feedstock for hydrogen and ammonia production.

|

|

While construction cost inflation has eased, costs remain elevated, creating pressures on project development. In addition, escalating U.S.–China trade tensions and higher global tariffs present a downside risk to export demand and resources investment, particularly if Chinese growth slows further.

|

|

|

|

|

|

|

Our most recent reports:

|

|

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|