|

|

|

|

|

|

|

New Macromonitor Forecasts for Residential Building

|

We have just finalised our latest forecasts for the residential building sector, with our new report on this segment due out this week. The key, short term factor at present is the positive impact of the HomeBuilder scheme, which is combining with other home buyer incentives and record low interest rates to drive a boom in detached house building.

|

We expect the number of detached house starts in calendar 2021 to be the largest number on record for a 12 month period, at almost 140,000, surpassing the previous record year of 1988/89. Multi-unit residential has not benefitted significantly from this boom, however, and remains in the cyclical downturn that followed the apartment boom of 2015 to 2018.

|

|

The boost to residential building has been particularly marked in regional areas. The number of total dwelling approvals is expected to increase in FY2021 by over 40% in non-metro regions, and by only around 12% in capital cities.

|

|

|

The HomeBuilder grant represents a larger proportion of the cost of a new dwelling in regional areas, and has therefore caused a more marked increase. And there has also been a large net movement of people from capital cities to regional areas since the onset of COVID-19.

|

The strength of house building, however, and the growth in regional areas in particular, is placing strains on home builders. We will likely see a more protracted lag from approvals to commencements, and to work done, than we typically see. And the rate of cost increases is also beginning to accelerate.

|

|

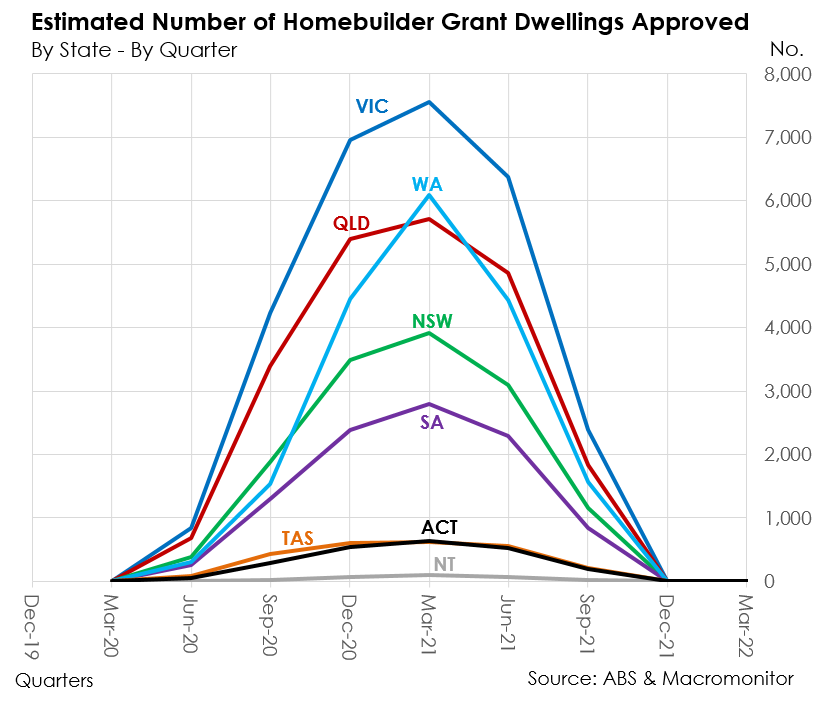

The states that have received the largest boost from HomeBuilder, relative to the existing level of building, are Tasmania and Western Australia, followed by South Australia and Queensland.

|

|

|

In terms of the number of houses approved, we expect the March Quarter 2021 will end up having been the peak quarter for approvals. The strength of house starts will be more protracted however. The number of house starts in the December quarter 2020 (the latest data we currently have) was close to 35,000 houses. We expect the number of starts will stay at around this level for 5 quarters, from December quarter 2020 to December quarter 2021 inclusive.

|

The critical time for the building cycle will be once this positive boost from HomeBuilder recedes. Then the second of our major influences – lower migration – will play a key role in determining how far activity falls.

|

Overseas migration each quarter has gone from a net inflow of around 60,000 people per quarter prior to the pandemic, to a net outflow 35,000 people per quarter now. And it appears overseas migration will be quite slow to rebuild, hopefully returning to relatively normal levels by late-2023. The big drop in migration will cause much lower occupant demand for dwellings (demand based on population growth), as shown in the chart below.

|

|

|

For Australia overall, we are forecasting a decline of 19% in total dwelling starts between the FY2021 peak and FY2023. After this downward correction, we anticipate another large upturn in dwelling building from FY2024 onwards, this time with both houses and multi-unit residential participating. This will be driven by the return of pre-pandemic levels of immigration, and an expected strong period of economic growth in Australia, with low interest rates likely to still be in place.

|

|

For more detailed forecasts and analysis, please see our new report - Australian Construction Outlook – Residential Building – June 2021.

|

|

|

|

|

Our most recent reports:

|

|

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|