|

|

|

|

|

|

|

Construction cost escalation eases, but sectoral pressures remain

Differences by project type and location mean tailored forecasts are essential

|

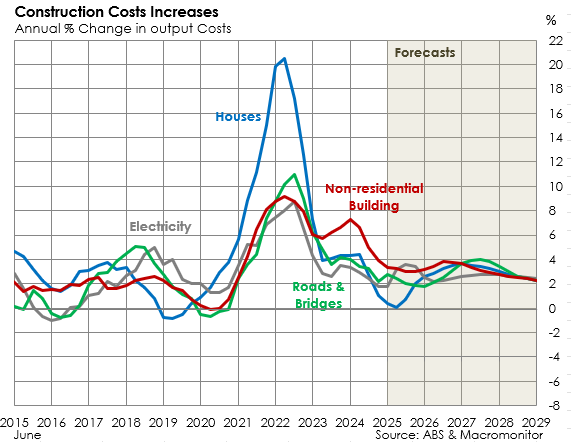

Overall construction cost escalation in Australia has moderated from the peaks of recent years, returning to more rate of growth. However, the pace of cost growth varies significantly across sectors. In 2024/25, cost escalation was just 0.3% in residential building, compared with 2.7% in roads and bridges and 3.3% in non-residential building (see chart below). These differences underscore the importance of understanding sector-specific cost drivers when planning projects.

|

Macromonitor continuously monitors cost escalation by input type, project type, and geographic region. We provide tailored escalation forecasts and rise & fall indexes to clients across a wide range of sectors. The projections in this newsletter represent an aggregation of that work.

|

The slowdown from the 2022 peak reflects easing global commodity prices, improved supply chains, and a relative improvement in labour and material availability. However, not all pressures have disappeared. The Australian dollar’s depreciation has placed a floor under the rate of cost inflation, offsetting some of these downward pressures. While the rate of cost growth has returned to more typical levels, overall cost levels remain significantly higher than in 2020 and continue to rise, albeit at a slower pace.

|

|

|

|

Looking ahead, costs pressures are expected to re-emerge as construction activity accelerates towards the next peak in 2027. Renewables, residential, and non-residential construction will all expand strongly, while high levels of transport infrastructure work will be maintained. These trends will place further pressure on materials and labour markets. Concrete, in particular, remains subject to strong demand and limited supply capacity, which is likely to drive above-average cost growth in this category.

|

During the peak construction period, a number of sectors are likely to see escalation rise to around 4%, or just below, before stabilising within a 2–3% band in the years that follow. Global trade uncertainty presents an additional risk factor. US tariff policies could push up costs for imported equipment and machinery, particularly in capital-intensive projects, while any slowdown in China — Australia’s largest trading partner — would weigh on exports and construction pipelines. This, in turn, could dampen demand for certain inputs and place downward pressure on prices in selected industries.

|

|

If you have a requirement for cost escalation forecasts, or rise and fall indexes, for specific projects, or for a range of work types, please get in touch with us to discuss.

|

|

|

Our most recent reports:

|

|

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|