|

|

|

|

|

|

|

|

Outlook and Impact of COVID-19 on Australian Construction Sector

|

|

|

The outlook for building and construction activity continues to evolve in the context of the COVID-19 pandemic, and the policy responses to it. Restrictions on travel and social gathering, in the various states and regions, have been through numerous permutations over recent months and remain in a state of flux. The policy responses, in particular, the additional spending by state governments aimed at stimulating recovery, are similarly continuing to develop.

|

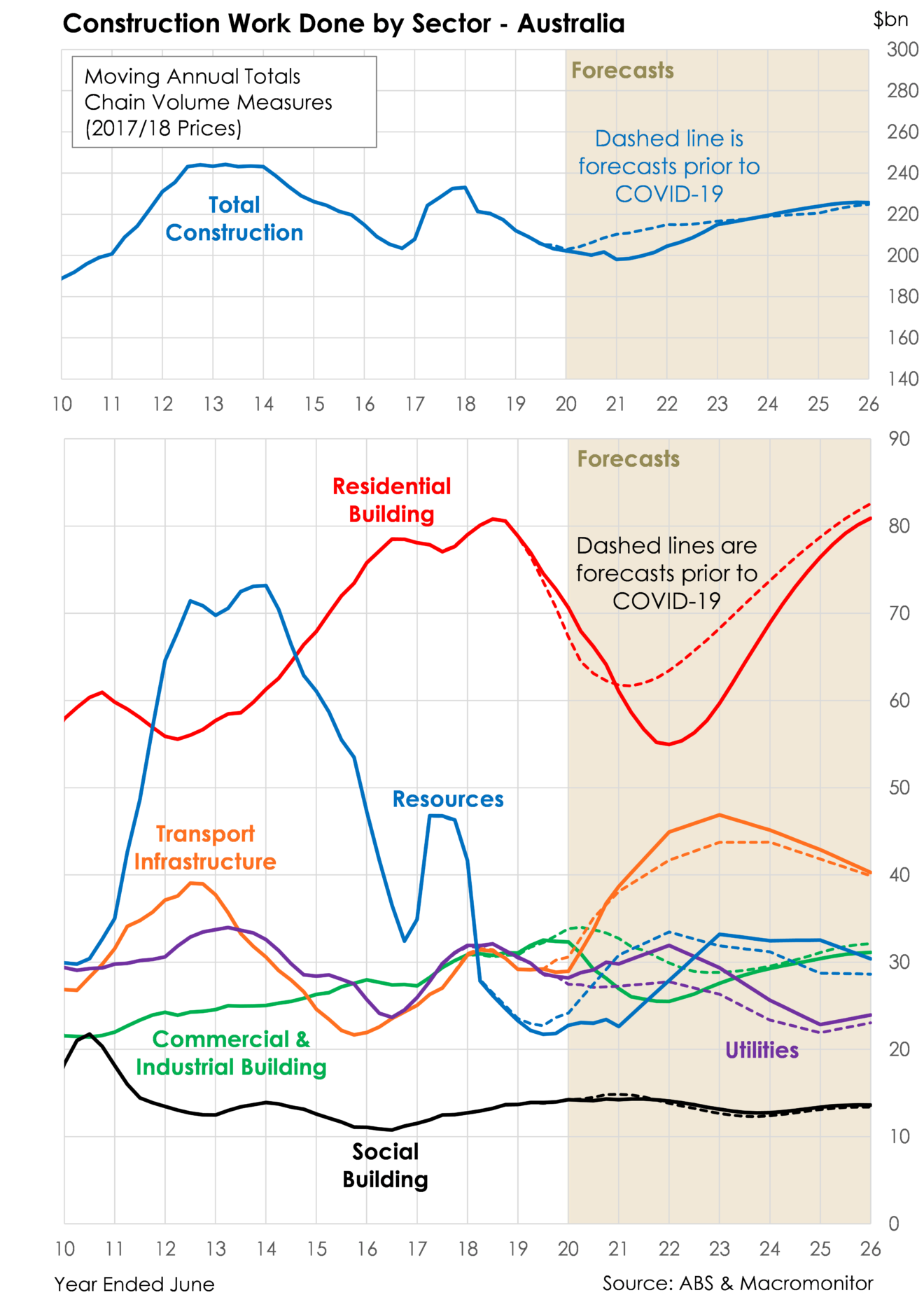

Our understanding of the impact of COVID-19 on the construction sector has evolved in a number of ways. Firstly, the impact up until the end of June 2020 was more limited than we initially feared it might be. Total construction activity dropped by around 4.6%, in real terms, in the year to June 2020, compared to the pre-COVID expectation of a 4.3% decline (implying a quite small COVID impact up to the end of June). The decline which was already underway prior to the pandemic was driven mainly by a residential building downturn which began in December 2018, combined with declines in renewable energy construction and falling levels of work on the NBN roll-out.

|

Macromonitor does expect some types of construction to actually be boosted higher than previously expected during 2020/21, due to additional spending and fast-tracking of projects. This has brought forward some demand in the short term and we now expect activity to fall by only 2% over the year to June 2021.

|

Thereafter, however, we don’t expect the rebound to be quite as strong, or quite as rapid, with a recovery expected to begin in 2021/22, and a return to previously expected levels by some time in calendar 2023.

|

Total construction work done in Australia in FY2020 was $200bn (in constant 2017/18 prices), which represents a drop of 4.6% on FY2019, and is 0.3% lower than we previously expected for FY2020.

|

We are then forecasting $198bn (again in constant 2017/18 prices) of total construction work done in Australia in FY2021, which represents a drop of 2% on FY2020, and is 6% lower than we previously forecasted prior to COVID-19 for FY2021.

|

Overall, the largest impacts will come from; sharply lower immigration and generally reduced movement of people, rising unemployment, reduced household incomes and confidence, much reduced utilisation of a range of building types, global downturns in the gas and other resources sectors, and a sharp contraction in the broader economy.

|

Macromonitor expects a rebound in total construction work done to start in 2021/22. Stimulus spending, combined with a degree of catch-up work, is expected to see total activity return to around its previously expected level by 2023.

|

|

Further discussion on each building and construction sector is available through our latest reports below. If you would like more information, or if you wish to subscribe, please visit the report pages.

|

|

|

Our most recent reports:

|

|

|

|

|

Australian Construction Cost Trends

|

|

|

This report examines the outlook for construction costs, in detail be sector and type of input.

|

|

|

|

|

|

|

|

Australian Construction Projects Database

|

|

|

This latest list of projects corresponds with our fully revised set of forecasts published in November 2023.

|

|

|

|

|

|

|

|

Australian Regional Construction Outlook

|

|

|

Our latest regional forecasts for residential building and construction have just been released.

|

|

|

|

|

|

|

|

Australian Construction Materials Forecasts

|

|

|

Our latest forecasts assess the implications for construction materials demand of the current outlook for building and construction.

|

|

|

|

|

|

|

|

Australian Road and Bridge Works

|

|

|

This report examines the strength and composition of the current upturn, and determines the likely timing of the peak, and subsequent decline.

|

|

|

|

|

|

|

|

|